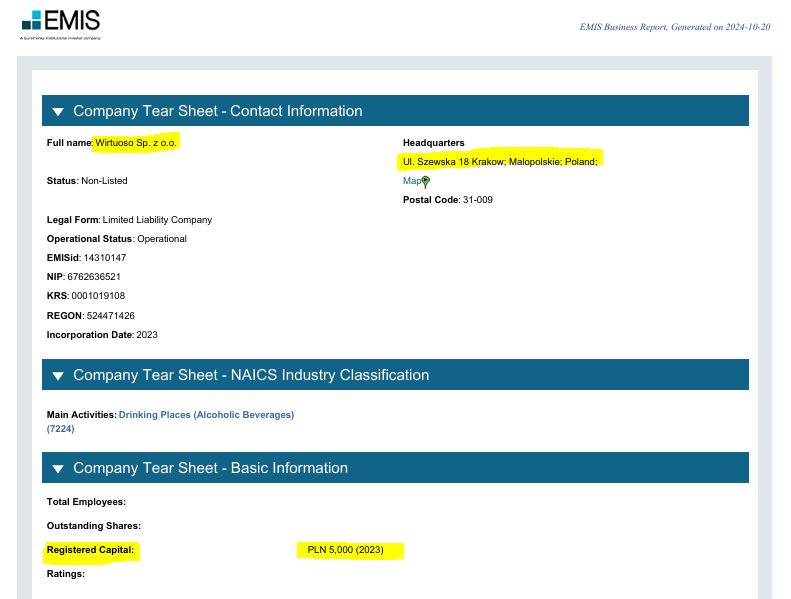

Wise approved over £13,500 GBP (~80,000 PLN) in wire transfers — in a single night — to a business whose only known financial disclosure was a 5,000 PLN registered capital. That’s the minimum required to incorporate a shell company in Poland. On paper, it met the legal threshold to exist — but not to process tens of thousands in international funds overnight.

This wasn’t just a formality — it should have been a red flag.

There was no verified business activity. No transaction history. No relationship to my account.

Instead of blocking or flagging it, Wise approved:

-

Three high-value wire transfers

-

Following 32 transactions in a 4-hour window

-

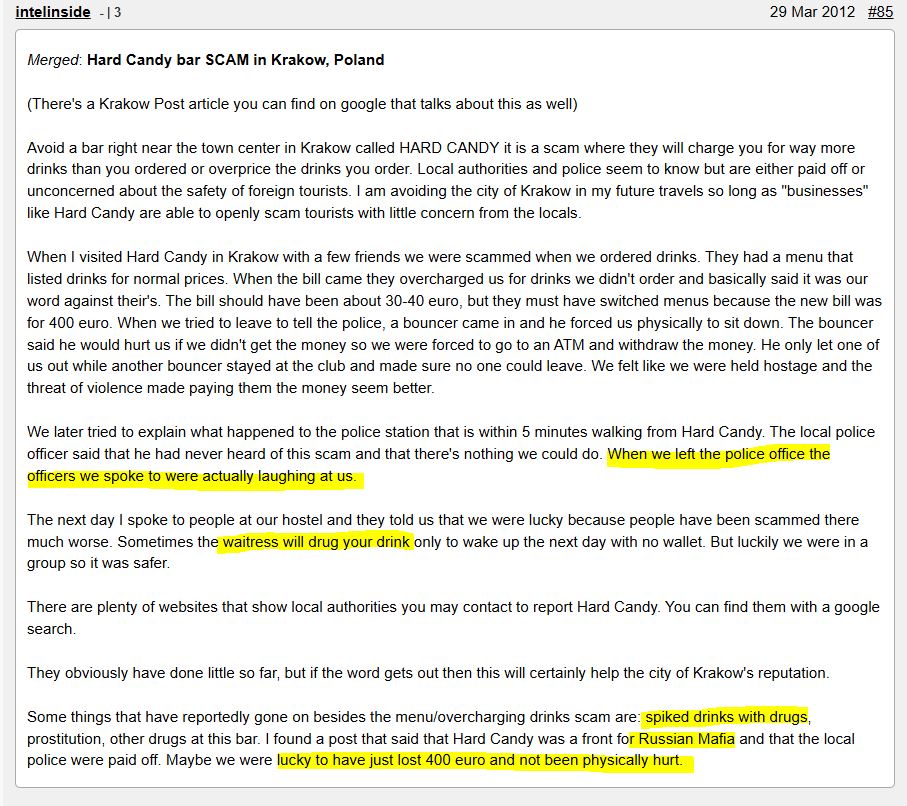

To a single entity linked to a known scam location in Kraków since 2009 – view review

Wise’s own AML (Anti-Money Laundering) obligations require them to flag suspicious activity — especially large transfers to low-profile or shell-like entities.

This company’s only financial footprint was 5,000 PLN. Yet Wise cleared over 16x that amount in a matter of hours.

If Wise had reviewed even the basic financial profile of WIRTUOSO SP Z O O, the fraud should have been instantly flagged and frozen.

Christopher Carson

Instead Wise:

Approved the transactions

Profited from currency conversion and transfer fees

Ignored public criminal warnings tied to this address

Closed my case with “no irregularities found.”

Why This Matters:

Tiny registered capital is a known fraud indicator in financial crime compliance.

Banks and fintechs are required under AML (Anti-Money Laundering) guidelines to check the legitimacy of recipient businesses.

Wise failed at one of the most basic due diligence checks.

What is AML?

Anti-Money Laundering (AML) laws are a set of international financial rules designed to:

Detect suspicious financial activity

Block criminal organizations from moving illegal money

Force banks and fintechs to know their customers (KYC) and verify recipients (KYB) before moving funds

Require companies to monitor unusual transactions and report them (called SARs: Suspicious Activity Reports)

How AML Applies to Wise

Wise, as a licensed financial institution in the UK, Canada, US, and EU:

Is legally required to have active AML monitoring systems.

Is legally required to flag and halt suspicious activity — not just after, but during a transaction cycle.

Is legally responsible for checking:

Where large money movements are going

If the recipient businesses are legitimate

If the flow of transactions matches the customer’s history

Wise owns the system. Wise wrote the rules.

Wise is obligated by law to stop irregularities.

AML Failures:

| Standard AML Expectation | What Wise Actually Did |

|---|---|

| Block suspicious new card issuance | Let new card be created after freezing original |

| Investigate multi-currency rapid transfers | Approved them without flagging |

| Review legitimacy of wire recipient | Wirtuoso SP Z O O with only 5,000 PLN registered capital |

| Monitor transaction timing (overnight, rapid-fire) | Let it all pass without manual review |

| Freeze account during sudden escalation | Never fully froze your account |

| Report potential fraud (SAR filing) | No evidence Wise filed anything |

{kind=link}

{kind=link}

Add comment