Email info@fintechfail.com

Wise Fraud Case – View My Case

Wise Fraud Case: Evidence, Timeline & Documents

“This wasn’t just a robbery. It was life-threatening — and Wise let it happen.”

My Wise fraud case took place on October 5th, 2024, I became the victim of a violent crime in Kraków. While I was incapacitated, Wise approved $25,861.68 CAD in unauthorized transactions including three wire transfers, multiple Google Pay tap payments, and associated currency conversion fees. This page documents the incident, Wise’s negligence, and the case I’ve built to hold them accountable.

Fintech Failed Me When It Mattered Most

While I was unconscious, Wise let the fraud play out. My card was frozen — then replaced. Wire transfers were approved. And when I asked for help, they told me to contact the place I was drugged and extorted. This isn’t a support issue. It’s a system failure.

This Is Not an Isolated

Incident

Before this case even launches publicly, I’ve seen the pattern. Customers ignored, fraud undetected, and zero accountability when it matters most. This isn’t just about my story — it’s about fixing a system that’s failing thousands.

What Happened:

A Timeline of the Night

Arrived in Krakow 7:47PM

Approached by a street promoter 9:52 PM

A quick Google search pulled up Pandora’s Box, a well-rated venue. So my friend and I went.

But the place we entered — also called Pandora — wasn’t it. It was a different venue at Ul. Szewska 18.

I believe they deliberately used the same name to mislead tourists. We weren’t just misdirected — we were set up.

I later learned this location previously operated as Hard Candy, a venue with a long history of scams, druggings, and robbery.

I documented all of this in my case to Wise — the name switch, the address, the venue’s past.

Ordered one drink 9:58 PM

However, shortly after consuming a single drink, I began to experience unusual and alarming symptoms, including extreme disorientation and physical discomfort.

The Witness: Thrown Out While I Was Being Held

At one point, he saw the manager, a woman who was seen moving in and out of the room I was being held in. He told her directly, “Please let my friend go, or will call the police..”

Her response? A smirk — as if to say, “Go ahead, try. No one will care.”

And she was right. No one did.

My friend eventually managed to get close enough to see me on the floor, half-naked and trying to crawl, slurring, asking “Where are my pants?”

He was immediately removed and physically ejected from the premises.

He called the police. He followed up. He waited. But no help arrived.

This entire interaction — including his attempt to get me out, the response from staff, and his contact with authorities — is documented in the official police report I submitted to Wise.

Assaulted, coerced to transfer funds 10:19PM-3:05AM

Over $25,000 CAD was withdrawn from my Wise account during the early morning hours. This included wire transfers, tap payments using Google Pay, and multiple currency exchanges —Wise financially benefited from criminal activity committed against me while I was incapacitated and under duress.

I don’t know exactly how access to my account was gained, but I suspect it involved coercion and the misuse of my phone’s facial recognition. I was drugged, disoriented, and vulnerable.

I remember only flashes: lying on the floor, trying to crawl, unable to speak. That’s the state my friend found me in — when he made it to the front of the room and saw me through the door.

That moment — face down, alone, and stripped of control — is the last thing I remember before waking up outside, in a park.

Discovered unconscious in a park 7:59AM

Reported to Wise via Wise App & Email 9:42AM

I truly believe this situation could have been prevented had Wise followed proper protocols or simply responded as their policy suggests.

(Every message, email, and timestamp is documented and available for review by media or legal professionals.)

Investigative Efforts & Final Response Breakdown

Following Wise’s initial denial of responsibility, I pursued every available avenue to escalate the situation — not just as a customer, but as someone determined to hold them accountable.

Final Decision: I received a “final response” from Wise, bundled with PDFs and legal disclaimers, suggesting the case was closed. Yet this decision ignored key evidence, timelines, and even Wise’s own public policies.

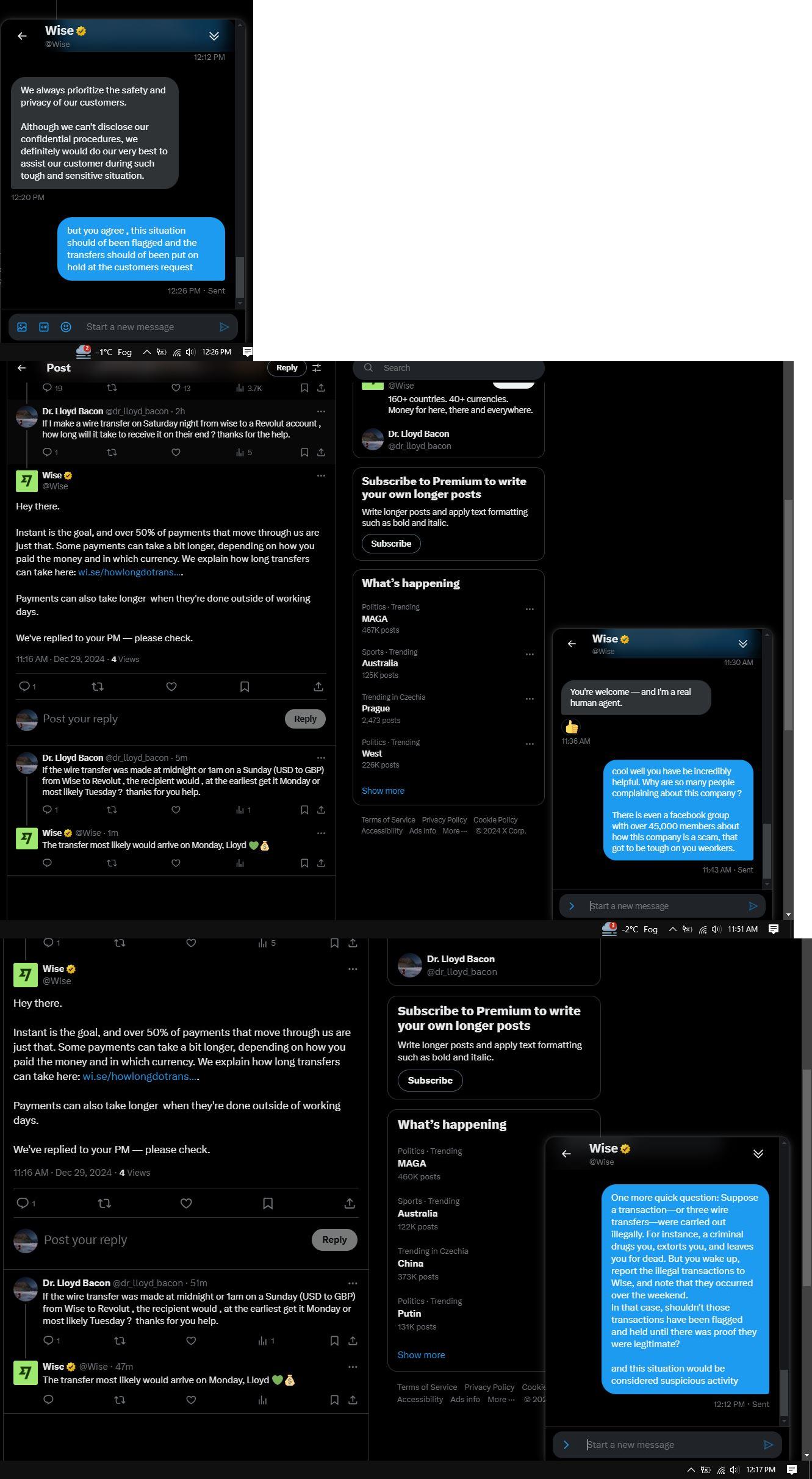

Twitter Confirmation: I was forced to create a Twitter account under an alias simply to engage with a Wise employee — something many customers claim is the only way to get a reply. Through this, I received confirmation that wire transfers take 1–5 business days. This means transfers initiated in the early morning hours of Sunday, October 6, could not possibly have reached the recipient (WIRTUZO SP Z O O / Revolut) that same day — as claimed.

“Wise acknowledged that weekend wire transfers take 1–5 business days. I reported the fraud within hours — yet no action was taken to stop or flag the transactions.”

@Dr_Lloyd_Bacon (Chris Carson)

{kind=link}

Attempting Direct Legal Contact: I then located internal Wise email addresses for their legal and regulatory teams and made direct contact, requesting someone from legal speak with me. I was instead redirected back to Niall — the same representative who authored the denial — who simply repeated the original outcome.

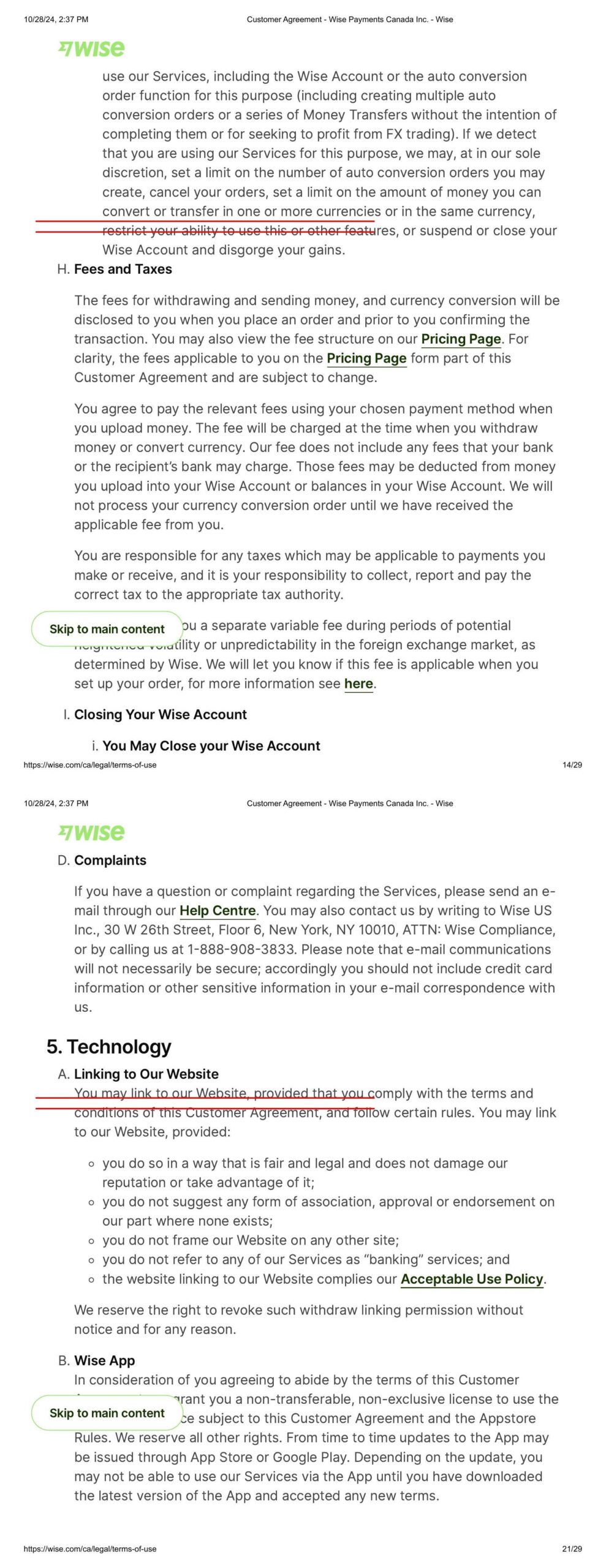

Contradictory Policy Clause: One clause in Wise’s own agreement — previously flagged — directly contradicts their dismissal of my case. It outlines that they are obligated to protect user funds and respond to security breaches or suspicious activity with immediate action. Wise failed to act on multiple fraud signals, including an overnight account drain, card reissue, and excessive currency exchanges.

This entire exchange demonstrates that not only did Wise dismiss me as a customer — they failed in their duty of care and violated their own consumer protections in the process.

“Wise will protect you from unauthorized activity and errors in your Wise Account. When this protection applies, Wise will cover you for the full amount of the unauthorized activity as long as you cooperate with us and follow the procedures described in this section.”

— Wise Customer Agreement – Wise Payments Canada Inc.

{kind=link}

"This isn’t about revenge. It’s about responsibility. I’m still here, and I’m not done fighting."

Christopher Carson

FintechFail.com exists to expose systemic weaknesses in digital finance platforms — and hold them accountable when lives are affected.

Have a similar experience?

I want to hear your story. Share it [here] or email me directly at info@fintechfail.com].

Want to share your story —

or join the fight for accountability?

If you've experienced unauthorized transactions or

inadequate support from Wise, you're not alone.